Kennedy Funding Lawsuit: The Total Borrower’s Handbook

Introduction

Hard money lending is typically viewed as the real estate investor’s lifeline when he or she requires quick cash to act on opportunity. One of the largest players in this field is Kennedy Funding Financial, LLC, a private lender whose reputation has been established on closing deals that would never be touched by a bank.

But with explosive growth and unorthodox practices, controversy is sure to follow. The Kennedy Funding lawsuit has gotten attention because it shows how fast the distinction between “alternative financing” and “predatory lending” can get fuzzy. To borrowers, it also brings questions: Were the conditions explained? Were the charges reasonable? And might they have steered clear of financial distress?

This guide breaks down the lawsuit in plain language. We’ll explore the company’s background, the allegations, how courts responded, and most importantly what consumers and businesses should take away from it. Have you checked our detailed guide on symmetry financial group lawsuit.

Who is Kennedy Funding?

Founded in 1987 and headquartered in New Jersey, Kennedy Funding carved out a niche in hard money loans. These loans are short-term, high-interest financing solutions often used by:

- Property developers racing against deadlines

- Investors who purchase troubled properties

- Borrowers who cannot qualify for bank financing because they have bad credit or insufficient documentation

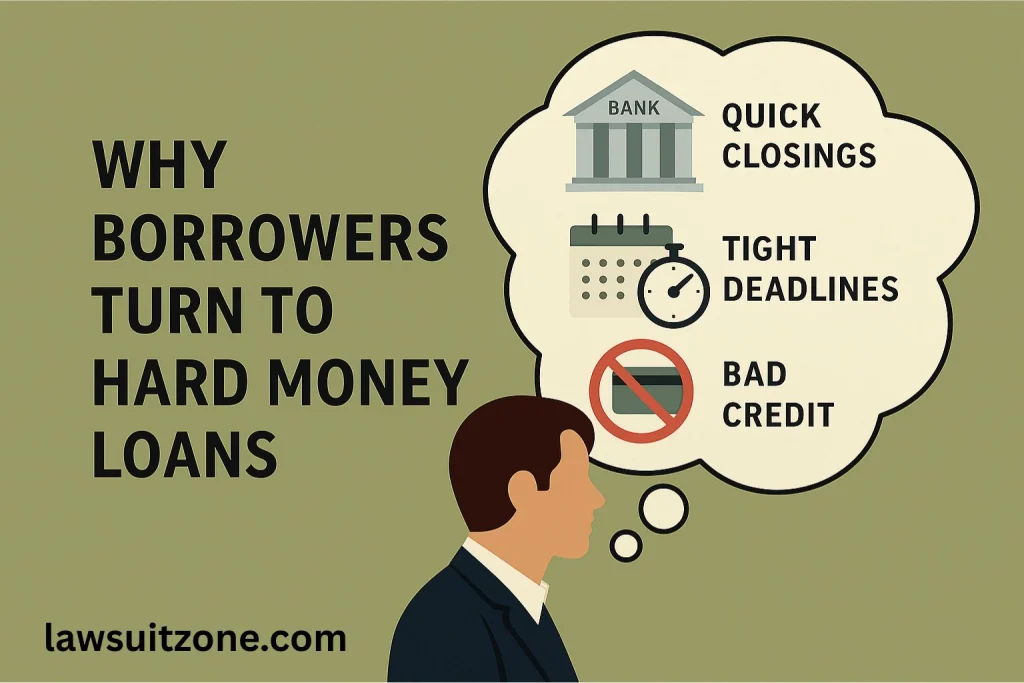

Why Borrowers Turn to Hard Money Loans

Traditional banks, which may take months to approve financing, are not where it’s at, according to Kennedy Funding. Speed and flexibility are the company’s hallmarks. Closings can be in weeks, and collateral is typically real estate holdings. The trade-off? Higher interest rates, hefty origination fees, and shorter repayment periods.

This “quick money at a price” scheme is precisely what draws in Kennedy Funding to some — and sparks controversy in others.

The Kennedy Funding Lawsuit: Why Was It Initiated?

The Kennedy Funding lawsuit is not one distinct case but a series of lawsuits and complaints that arose over the years. Business partners and borrowers have complained of the lender’s unfair business practices, concealed fees, and swift foreclosure proceedings.

Allegations at the Heart

Deceptive Terms of the Loan

Plaintiffs claimed Kennedy Funding misled them on repayment terms, interest rates, and collateral. What was once a sustainable loan became unmanageable.

Unspecified or Excessive Fees

A number of suits alleged application fees, due diligence fees, and origination fees that were explained insufficiently. Borrowers in certain suits claimed fees devoured a considerable amount of their funding.

Predatory Lending Practices

Critics argued Kennedy Funding preyed upon distressed borrowers who had few choices, trapping them in terms that almost assured default.

Foreclosure Disputes

Several of the cases included borrowers charging that Kennedy Funding acted too hastily to take back collateral properties, sometimes during negotiations.

Kennedy Funding’s Response

Kennedy Funding has denied wrongdoing in the suits consistently. Its defense hinges on a few points:

- All loan terms are in written agreements that have been signed.

- Borrowers are highly sophisticated parties who grasp the dangers of hard money loans.

- The firm serves a vital market niche by lending on projects banks won’t touch.

In short, the Kennedy Funding stance is that it lends in high-risk situations, and such risks are known — and accepted — by borrowers prior to loan closing.

The Legal Proceedings

The lawsuit against Kennedy Funding has experienced a varied set of outcomes across jurisdictions.

Court Findings

- Some courts had dismissed cases in favor of Kennedy Funding on the grounds that loan documents clearly revealed fees and payment terms.

- In some others, courts permitted claims to go forward when facts indicated that the borrowers had been deceived or terms were not clearly explained.

Settlements

Some conflicts were settled, and this usually involved money payments to borrowers. Notably, these settlements were usually resolved without Kennedy Funding’s liability being acknowledged.

Though settlements avoid lengthy court battles, they also highlight the fact that Kennedy Funding was under enough legal pressure to negotiate.

Impact on Borrowers

To those who did business with Kennedy Funding, the lawsuit presents a dismal scenario.

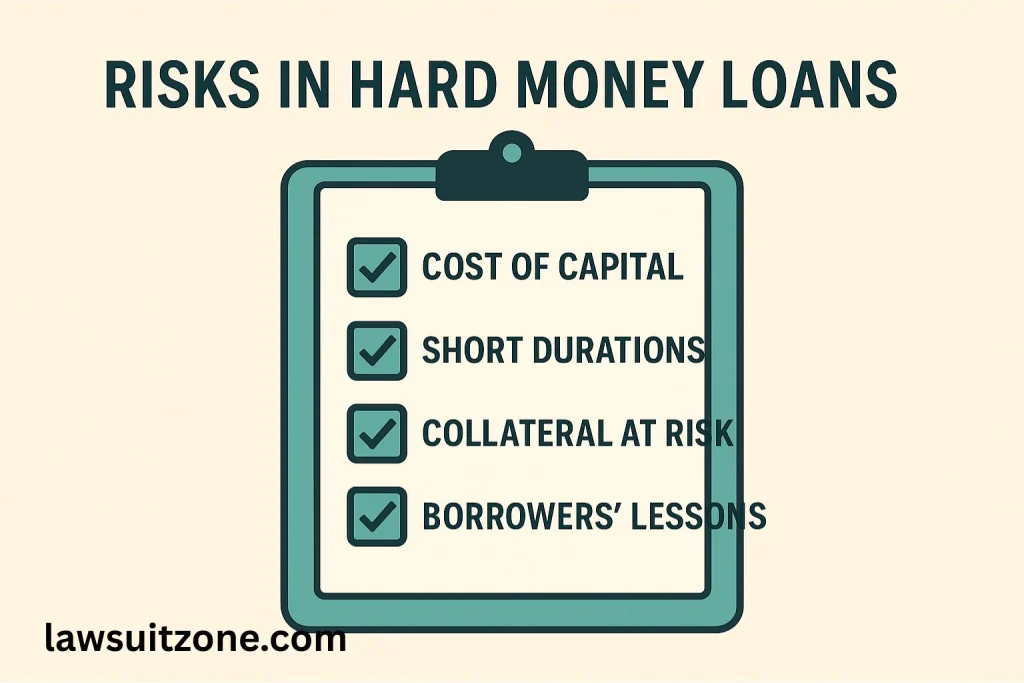

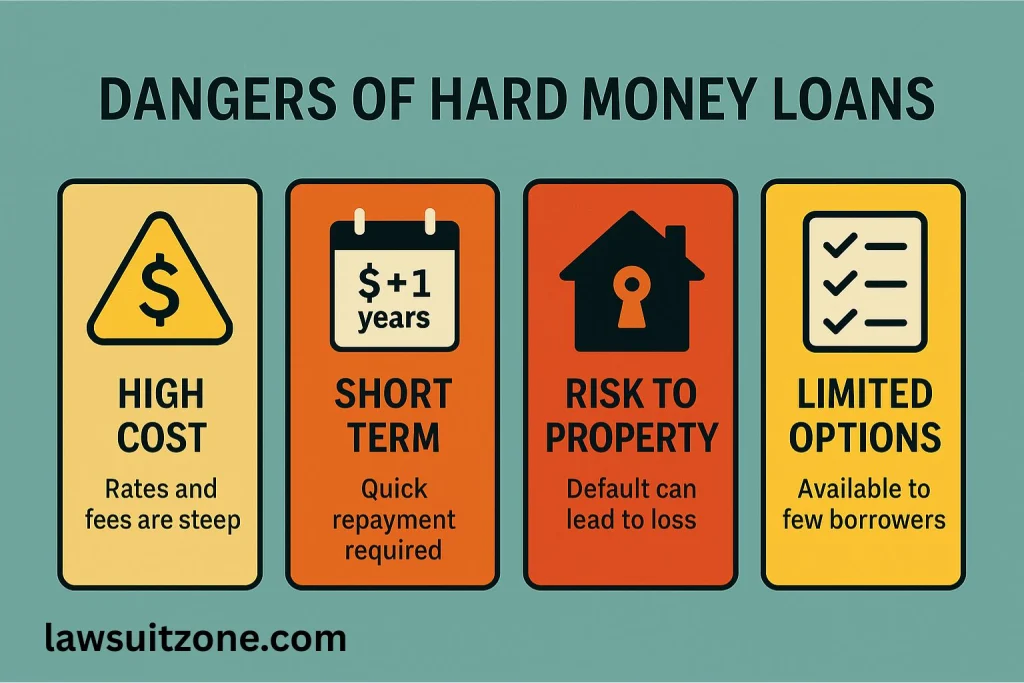

Borrower Risks in Hard Money Lending

- Cost of Capital: Rates and fees are considerably higher than bank loans.

- Short Durations: Repayment is usually expected within 1–3 years.

- Collateral in Jeopardy: Default may mean quick loss of prized assets.

Borrowers’ Lessons

- Read Contracts Carefully: Never gloss over loan contracts. Each term is important.

- Seek Professional Assistance: A lawyer or financial counselor can identify risks the borrower might overlook.

- Plan Your Exit: Hard money loans are only successful if you know precisely how you will repay them.

- Compare Options: Even if rushed for time, borrowers must shop around among several lenders.

For advice on how to recognize predatory lending practices, the Consumer Financial Protection Bureau (CFPB) provides tools that may enable borrowers to steer clear of predatory deals.

Wider Consequences of the Kennedy Funding Lawsuit

The lawsuit is larger than the company. It identifies systemic problems in private lending.

Regulatory Responses

- State regulators have stepped up regulation of non-bank lenders.

- There’s pressure to compel more transparent disclosures within loan agreements.

- There are ongoing debates about capping some fees in hard money lending.

Reputation of Private Lending

Even though Kennedy Funding is still functional, such lawsuits have left private lenders with an unfavorable reputation. Borrowers are now looking to them as a last resort, which could push the industry towards more open practices.

Lessons for Businesses

The Kennedy Funding lawsuit serves stern lessons for other lenders and businesses.

Transparency Builds Trust

Concealing fees or hiding them in the fine print can result in lawsuits and damage to reputation.

Compliance is Non-Negotiable

Businesses are required to comply with state and federal lending regulations, including policies issued by the FTC and CFPB.

Protect Reputation

Negative publicity goes viral quickly in the electronic age. Honest lending practices are not only the law but also brand imperatives.

Customer-Centric Models Win

Sustained business success is based on building relationships, not on taking advantage of vulnerabilities.

The Human Side of the Kennedy Funding Lawsuit

Behind the court documents are true accounts of borrowers who entrusted a lender and ended up feeling deceived. Some borrowers told how they lost properties they had put years of effort and money into. Others told how charges took so big a chunk out of their money that they left them with little to spend on their projects.

These tales serve to illustrate the purpose of consumer protection: financial agreements have the power to alter the course of businesses and families, for good or ill.

The Future of Kennedy Funding

In spite of court battles, Kennedy Funding is still a major hard money lender. The fact that it continues to thrive confirms the demand for quick, alternative funding remains.

Potential Directions Forward

- More Regulation: Regulators can bring new regulations to private lenders.

- Transparency of Contracts: Borrowers might require more transparent, streamlined contracts.

- Reputation Recovery: Kennedy Funding will need to consciously rebuild trust through better practices and dialogue.

Frequently Asked Questions (FAQs)

Conclusion

The Kennedy Funding lawsuit is a reminder of the dangers and realities of borrowing beyond conventional banks. It serves as a reminder of how important transparency, compliance, and fairness are in financial transactions.

For borrowers, the message is clear: read all contracts, take professional advice, and be aware of the risks involved in short-term, high-rate loans. For companies, the case demonstrates that long-term success is based upon trust, transparency, and ethical business practices.

In the end, the Kennedy Funding lawsuit demonstrates that although hard money lending can be a useful tool, it must be used with caution and responsibility by both parties.