National Life Group Lawsuit: 2025 Consumer Guide

National Life Group Lawsuit: A Complete Consumer Guide

The National Life Group suit has been on everyone’s lips among investors, retirees, and policyholders nationwide. Why? Because when a household name in insurance and financial planning comes under legal fire, people get nervous. Investors who put their money in the company or purchased insurance policies want to know: What does this mean for me?

This handbook explains the lawsuit from all sides company background, claims, customer experiences, court process, potential outcomes, and real-life lessons for defending yourself. Have you checked our detailed guide on Tampax Lawsuit.

Who is National Life Group?

National Life Group is not a newcomer—it’s a financial giant with origins dating to 1848. Throughout the generations, it has sold itself as a trusted partner for:

- Life insurance

- Retirement savings plans

- Annuities

- Wealth protection services

To countless families, the company has meant stability and good conscience. Even long-established institutions, however, can find themselves in court when questioned about their practices. The National Life Group lawsuit serves as a reminder that reputation is no guarantee of ethical behavior.

Why Financial Companies Get Sued

Financial lawsuits are commonplace. They typically happen when customers feel they’ve been misled, overcharged, or sold something inappropriate. Typical reasons include:

- Misrepresentation – Return promises that fail to live up to their words.

- Hidden Fees – Unexpected fees hidden in fine print.

- Unsuitable Investments – Conservative or older investors urged into high-risk products.

- Breach of Duty – Advisors who don’t put the client’s best interests first.

- Aggressive Sales Tactics – High-pressure sales strategies that confuse consumers.

The National Life Group lawsuit illustrates several of these themes.

How Did the National Life Group Lawsuit Begin?

Complaints started to emerge from retirees and policyholders. Some claimed they had been induced to purchase costly life insurance policies or annuities that did not suit their requirements. Others asserted that they were not informed of surrender charges or long-term risks.

Lawyers collated these narratives and contended that National Life Group’s sales tactics were deceptive. The case expanded to a large suit shortly.

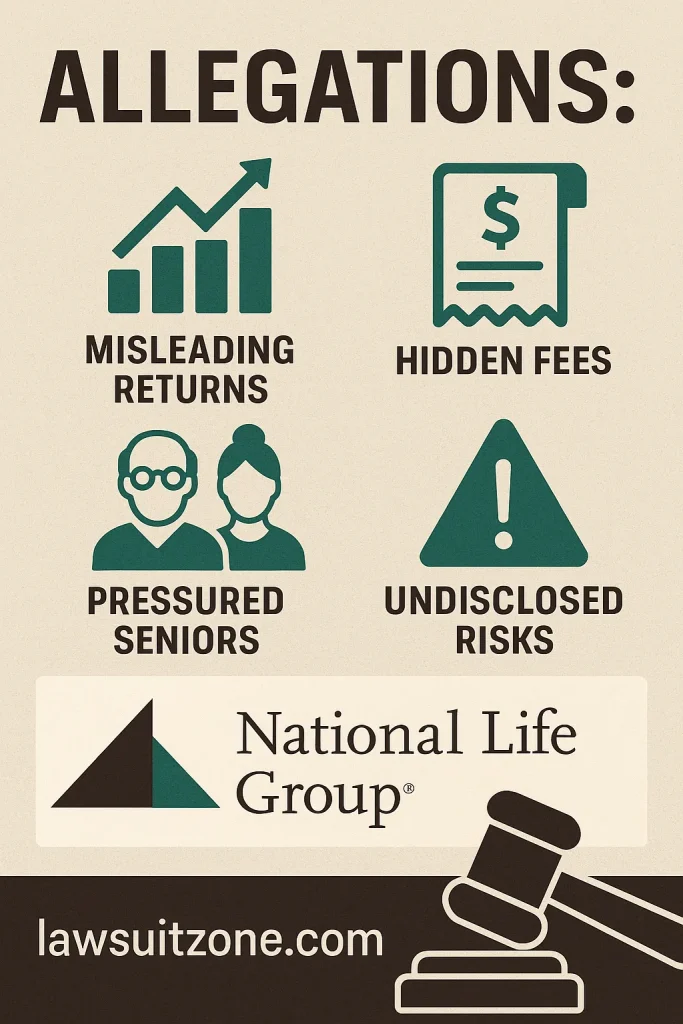

Major Claims in the Suit

The National Life Group lawsuit centers on:

- Misleading Returns – Advertised expected greater returns than were actually achievable.

- High-Cost Products – Customers pressured into contracts with hefty premiums that depleted savings.

- Lack of Transparency – Significant fees and penalties buried in contracts.

- Targeting Seniors – Senior retirees targeted as allegedly pressured into products unsuitable.

- Failure to Disclose Risks – Customers report risks not well explained.

The Legal Process Step by Step

Here’s the way lawsuits of this nature usually go:

- Complaint Filed – Plaintiffs (investors/policyholders) file their case.

- Response – National Life Group files its defense.

- Discovery – The two sides swap evidence and testimony.

- Negotiation – A large number of lawsuits are settled prior to going to trial.

- Trial (if necessary) – A judge or jury determines whether the company is at fault.

It can take several years, and results often hinge on how much evidence plaintiffs can establish.

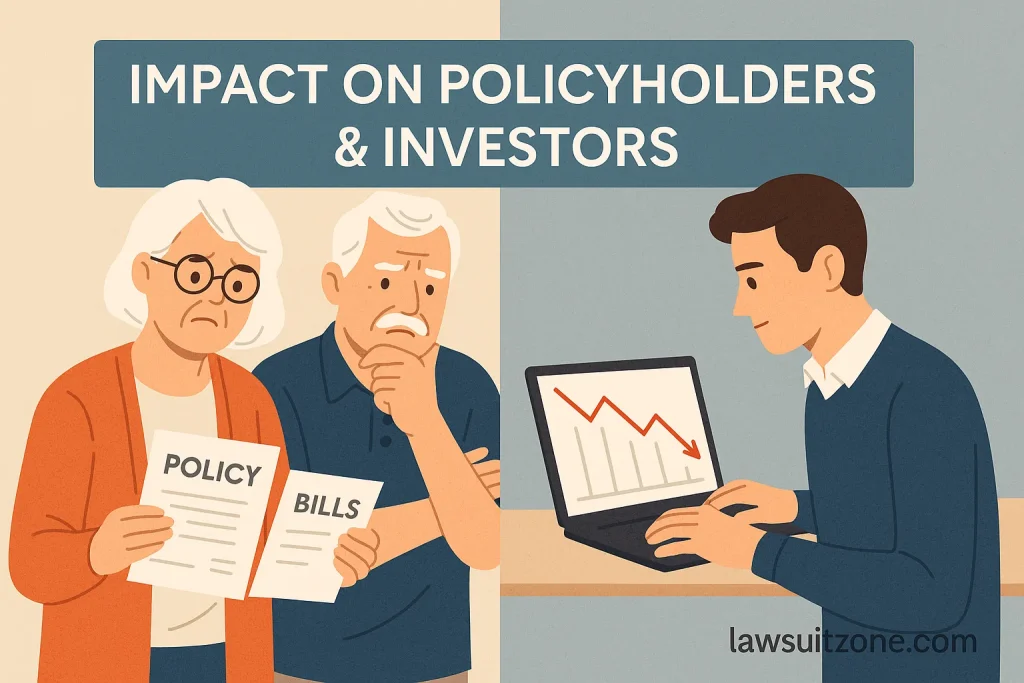

Impact on Policyholders and Investors

The National Life Group suit doesn’t imply instant customer financial loss, but it does pose questions:

- Policyholders will question whether their premiums were spent inappropriately.

- Retirees who depend on annuities will worry about payments or secret charges.

- Investors might observe the company’s reputation—and stock performance—hurt.

Though the case may continue, the fact that it was filed causes distress for customers who trusted the name.

Lessons from the Lawsuit

For ordinary folks, this suit offers important lessons about money:

- Ask tough questions prior to signing any annuity or policy.

- Demand detailed fee breakdowns—no summaries.

- Review whether products suit your age, objectives, and risk capacity.

- Think about getting independent advice rather than depending on the company representative alone.

Consumers’ Stories

Numerous policyholders who signed on to the lawsuit say they were pressured in sales presentations. Some reported being informed their annuities would earn them great returns with “minimal risk.” Others found that when they attempted to cash out, surrender fees erased a large chunk of their savings.

These anecdotes explain why the National Life Group lawsuit isn’t about forms—it’s about human beings and their retirement aspirations.

Comparisons to Similar Lawsuits

This case is not an isolated one. Other big-name financial institutions have been sued for doing the same thing:

- MetLife – Misrepresentation of pension calculations.

- Prudential – Sued for deceptive sales practices.

- Allianz – Sued for inappropriate annuity recommendations.

Traits common to these cases show one thing: consumers need to be wary, even of “big name” firms.

Probable Outcomes of the National Life Group Lawsuit

The suit may have a number of different outcomes:

- Settlement – The company pays damages without an admission of fault.

- Court Ruling – Judge or jury awards damages.

- Dismissal – Case can be dismissed if evidence isn’t sufficient.

- Reform – National Life Group can be compelled to alter policies and become more transparent.

How Consumers Can Protect Themselves

As the case develops, here’s what you can do:

- Stay abreast of developments in financial news.

- Watch your accounts for suspicious charges.

- Diversify investments to minimize risk exposure.

- Report the concerns to regulators such as the U.S. Securities and Exchange Commission (SEC) in case you suspect any misconduct.

Frequently Asked Questions (FAQs)

Final Thoughts

The National Life Group suit isn’t merely about legal allegations—it’s about trust. When financial institutions that deal with individuals’ life savings come under fire, consumers are entitled to insist on the truth.

Whether the case settles or makes it to the courtroom, one point is certain: protect yourself at all times with information, inquire about things, and never execute financial contracts without complete knowledge.

For today’s customers, the case is a wake-up call: your money future is too valuable to be left in someone else’s hands without responsibility.