How Do I Get Out of Debt in Texas?

If you are asking how do I get out of debt in Texas, you are asking the right question at the right time. Texas ranks number one in the country for financial distress in 2026, and bankruptcy filings nationwide jumped 14% in the first quarter of this year alone. You are not failing. The numbers prove that millions of Texans are in the same position right now, and there are real, legal options available to you today.

Getting out of debt in Texas depends on how much you owe and what type of debt you carry. Options range from debt consolidation and negotiation to bankruptcy, which can eliminate most unsecured debt entirely. For many Texans, bankruptcy is the fastest and most complete solution available — and Texas law protects your home, car, and retirement accounts throughout the process.

This guide breaks down what Texans owe, which types of debt are hitting hardest, and what your actual options are for getting out from under it.

Why So Many Texans Are Struggling With Debt Right Now

Texas leads the nation in financial distress according to WalletHub’s most recent state rankings. That is not a coincidence. Several forces are hitting Texas households at the same time in 2026.

Credit card debt in the United States just surpassed $1 trillion for the first time in history. The average Texas household carries more credit card debt than the national average. On top of that, student loan collections restarted in 2025 after a multi-year pause. Tariffs pushed grocery and consumer goods prices higher. And insurance costs for homes, cars, and health rose sharply across the state.

Texas also has one of the highest rates of medical debt in the country. Unlike most states, Texas has not expanded Medicaid. That means lower-income Texans who get sick often have no coverage and face the full cost of hospital and doctor bills out of pocket. Medical debt is now one of the top three reasons Texans file for bankruptcy.

The Four Types of Debt Hitting Texas Hardest

Not all debt is the same. Understanding what you owe helps you figure out which solution fits your situation.

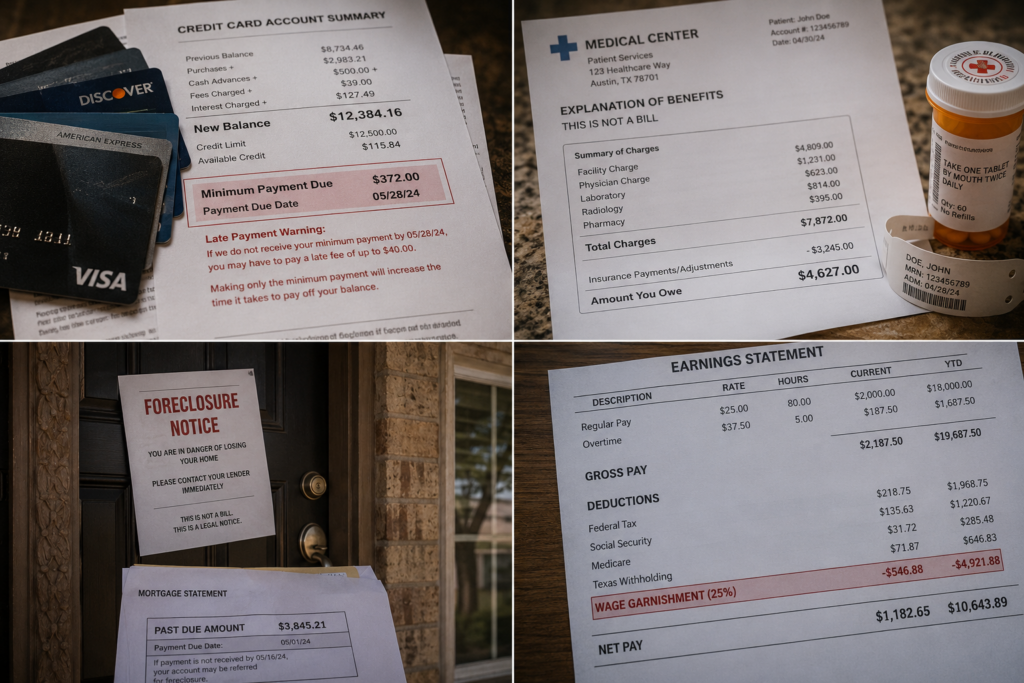

Credit card debt. This is the most common source of financial distress for Texas households. High interest rates often between 22% and 29% mean balances grow faster than minimum payments can shrink them. A $15,000 credit card balance at 24% interest can take over 20 years to pay off making minimum payments. Bankruptcy eliminates credit card debt entirely in most cases.

Medical debt. Texas hospitals and healthcare providers are among the most aggressive collectors in the country. Medical bills can go to collections within 60 to 90 days of going unpaid. A single emergency room visit, surgery, or hospital stay can produce a bill of $20,000 to $100,000 or more. Medical debt is fully dischargeable in bankruptcy.

Wage garnishment. When a creditor wins a lawsuit against you in Texas, they can garnish up to 25% of your disposable income. That means one in four dollars from every paycheck goes directly to the creditor before you ever see it. Filing bankruptcy triggers the automatic stay, which stops wage garnishment the same day you file.

Mortgage and foreclosure pressure. Rising home insurance costs and property taxes are pushing Texas homeowners behind on their mortgages even when they were current just a year ago. Foreclosure proceedings can begin after just one missed payment in some cases. Chapter 13 bankruptcy stops foreclosure immediately and gives you three to five years to catch up on missed payments while keeping your home.

What Are Your Options for Getting Out of Debt in Texas?

There is no single answer that works for every situation. Here is an honest breakdown of your main options and when each one makes sense.

Debt consolidation. This works when your total debt is manageable, usually under $15,000 to $20,000, and you have enough income to make consistent payments at a lower interest rate. You combine multiple debts into one loan. The problem is that consolidation does not reduce what you owe. It just reorganizes it. If your income cannot cover the consolidated payment, it fails.

Debt settlement. A settlement company negotiates with your creditors to accept less than the full balance. It sounds good, but the math is tricky. Settlement companies charge fees of 15% to 25% of the enrolled debt. While you are saving up for settlements, you stop making payments, which tanks your credit and opens you up to lawsuits. There is no guarantee creditors will agree. Any forgiven debt may also be treated as taxable income by the IRS.

Chapter 7 bankruptcy. This is the fastest path to eliminating unsecured debt. Credit cards, medical bills, personal loans, and payday loans are discharged in 90 to 120 days. Most Texas filers keep everything they own because Texas has some of the most generous exemption laws in the country. The homestead exemption protects your home with no dollar cap. One vehicle per licensed household member is fully protected. Retirement accounts are fully exempt.

Chapter 13 bankruptcy. This is the right path if you are behind on mortgage or car payments and want to keep those assets. Chapter 13 creates a three-to-five-year repayment plan based on what you can actually afford. At the end of the plan, remaining qualifying debt is discharged. It stops foreclosure immediately and lets you catch up on missed payments over time.

What Texas Law Does to Protect You When You File

Texas debtors have some of the strongest legal protections in the United States. Most Texans who file bankruptcy are surprised by how much they get to keep.

- Homestead exemption: Protects your primary residence with no dollar cap on value, as long as it sits on 10 acres or less in an urban area

- Vehicle exemption: One vehicle per licensed household member, fully protected regardless of value

- Retirement accounts: 401(k)s, IRAs, pensions, and profit-sharing plans are fully exempt

- Personal property: Up to $50,000 for a single filer or $100,000 for a family in household goods, clothing, and personal items

- Wages: Current unpaid wages are exempt from most creditor claims

These protections mean that for the vast majority of Texas families, filing bankruptcy does not mean losing what matters most. It means eliminating the debt that is preventing you from moving forward.

How Do You Know If Bankruptcy Is the Right Answer?

Bankruptcy makes the most sense when the math no longer works. Here are the clearest signals that it is time to talk to an attorney.

- You use credit cards to pay for groceries, utilities, or other monthly necessities

- You make minimum payments but your balances keep growing

- You have received a lawsuit, judgment, or wage garnishment notice

- You are behind on your mortgage or car payments and at risk of losing them

- Your total unsecured debt exceeds what you could realistically pay off in three to five years

- You have medical bills you have no realistic path to paying

Take the Next Step

If two or more of the warning signs above describe your situation, the next move is a conversation with a bankruptcy attorney. Thousands of Texans asking how do I get out of debt in Texas find that a free 30-minute consultation gives them a clear picture of exactly where they stand, what is protected, and what their fastest path forward looks like. The sooner you get that information, the more options you have.